Enter your email below to receive weekly updates from the Ashton College blog straight to your inbox.

By: Ashton College

Published On: December 13, 2017December is the month that brings attention to financial matters. The abundance of financial literacy events from the month before and closeness to the new year makes December an ideal month to ask yourself: what money-related habits should I change to get ahead?

It is fair to say that every single person wants to succeed in life. Although success means different things to different people, each person’s definition of success usually incorporates three of the following categories:

We have heard multiple times that financial gain is not the main ingredient in success or happiness. However, it is hard to deny that all of us want to at least reach the state of financial stability, if not financial abundance. We live in an expensive world: most of our basic necessities (food, shelter, etc.), hobbies, aspirations (education, career training, etc.), and even helping and charitable actions require money. That does not mean that our main goal should be making millions, but let’s be realistic about one fact:

Being in control of your finances leads to having more freedom and more options in life.

Steve Fooks, a Certified Executive Coach and a Financial Services instructor at Ashton College, takes this idea even further, pointing out the importance of a debt-free lifestyle. “In North America, it is quite easy to start spending money that you don’t have, with no plan of financial return. Because of that, people get in debt when they are younger, and then spend years trying to pay off debts just to get to point zero. This is where financial planning comes in: it helps people not only plan for their future, but also to save up for their past.”

It always feels better to spend money that you have rather than stress out about loan or debt payments. The sooner you start planning ahead and thinking about your spending, saving and investing habits, the more peace of mind you will have and the better your results will be.

Earlier in November, Ashton College held a Financial Literacy Workshop with Steve Fooks. Throughout the event, Steve shared his wisdom and key tips on how students can start making better financial decisions. In this feature, we point out the key ingredients from the workshop that will help you take your finances under control and move towards effective money management and financial stability.

In order to develop healthy money habits, you need to start with education.

Think about it: we spend years and years in school, taking notes, reading textbooks and learning as much as we can about each subject in order to get our degree. But when it comes to life skills, personal development and financial matters, how many of us actually take the time to learn from industry professionals and educate ourselves?

“Remember that financial intelligence is the mental process via which we solve our financial problems.” – Robert Kiyosaki

Financial literacy and financial education are vital to wealth management. Learning from people who took their time and energy (and money, if you are learning about investments) to test different tools and strategies can help you better understand which route to take to avoid the mistakes that others made and to maximize your gains.

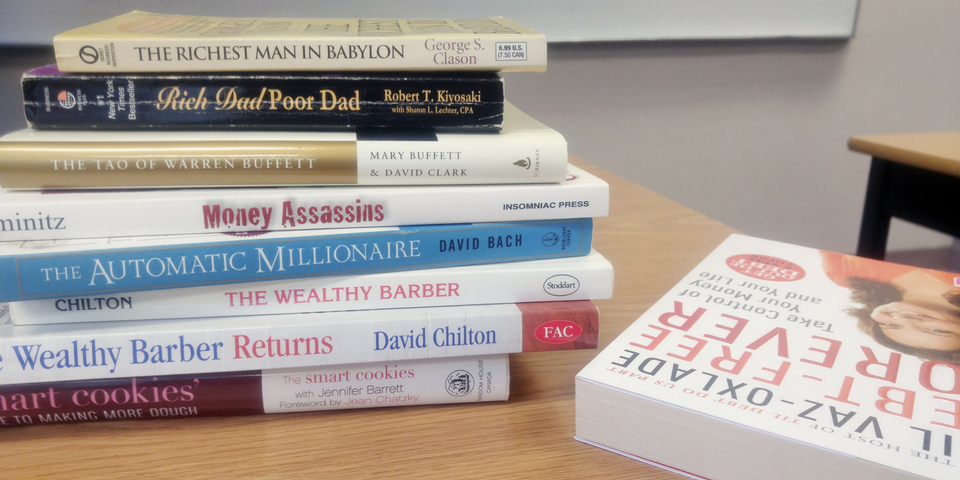

If you are serious about taking your financial education seriously, a good place to start is learning from financial gurus. Steve Fooks recommends several books by Robert Kiyosaki, David Chilton and Warren Buffet that will start you on the right path towards financial enlightenment. It is literally a pile of wisdom and a valuable list of reads to educate yourself on money management.

One of the key ingredients in money and wealth management is your mindset, or your attitude. Budgeting is a great example of this. If you believe that budgeting is hard, it will be difficult for you to stay on budget. You will find it restricting, will think of it as a burden, and will likely not follow it.

On the other hand, if you believe that budgeting is necessary for your future goals, you will continuously remind yourself of the bigger picture and the reasons for following the budget. Those reasons can be diverse: getting out of debt, saving up for a big purchase, focusing on investing your money, etc. If you keep the long-term vision in mind, you will see that budgeting gives you the freedom to stay in control and spend your money how you want to spend it.

We can come back to budgeting in the next section. In the meantime, here are three key tips to help you develop the right attitude towards money management:

“The great secret to getting rich is getting your money to compound for you.” – The Tao of Warren Buffett: Warren Buffett's Words of Wisdom

Let’s clear the misconceptions about budgeting: it is not a constraint on spending or activities, but as a way to review and organize your spending. A budget simply tells you what you can and cannot afford and helps you understand and determine where your money goes.

Let’s clear the misconceptions about budgeting: it is not a constraint on spending or activities, but as a way to review and organize your spending. A budget simply tells you what you can and cannot afford and helps you understand and determine where your money goes.

Creating a budget is the first step on the road towards financial freedom. Sticking to your budget is perhaps the most common challenge. At the same time, your attitude towards money will determine your financial future.

The first step of any budget is to ensure that your expenses do not exceed your income. If you have never had a budget before, a good place to start is breaking down your current spending habits.

Now that this is done, it’s time to ask tougher questions. What are your goals, both short-term and long-term? What would you like to achieve in the next few years? Are there any large purchases coming up in the near future? Those would be the questions that will guide your future spending, saving and investment.

If you are unsure how to create the budget that would best work for your future plans, you could always make an appointment with a financial adviser. Their main goal is to help you create and solidify a financial plan that would help you effectively reach your goals. Try it out! It might be more beneficial than you think.

The information contained in this post is considered true and accurate as of the publication date. However, the accuracy of this information may be impacted by changes in circumstances that occur after the time of publication. Ashton College assumes no liability for any error or omissions in the information contained in this post or any other post in our blog.