Are You Spending Your Personal Income Effectively? | Infographic

By: Alex Nikotina,Ludmila Soares

Published On:

November 6, 2017

Budgeting can seem like a dreadful world for many people. If that is the case for you, you probably are thinking of a budget as something difficult, restricting and undesirable. In reality, budgeting is none of those things.

A budget is simply a way to plan where your money goes and to be aware of your income, spending and saving habits. It gives you an opportunity to ensure continuous cash flow, make arrangements for larger purchases and life changes, and save up for the future or for emergency situations. Budgeting is a way to keep your finances on track and make sure that your income is not below your expenses.

Don’t know where to start? We can help!

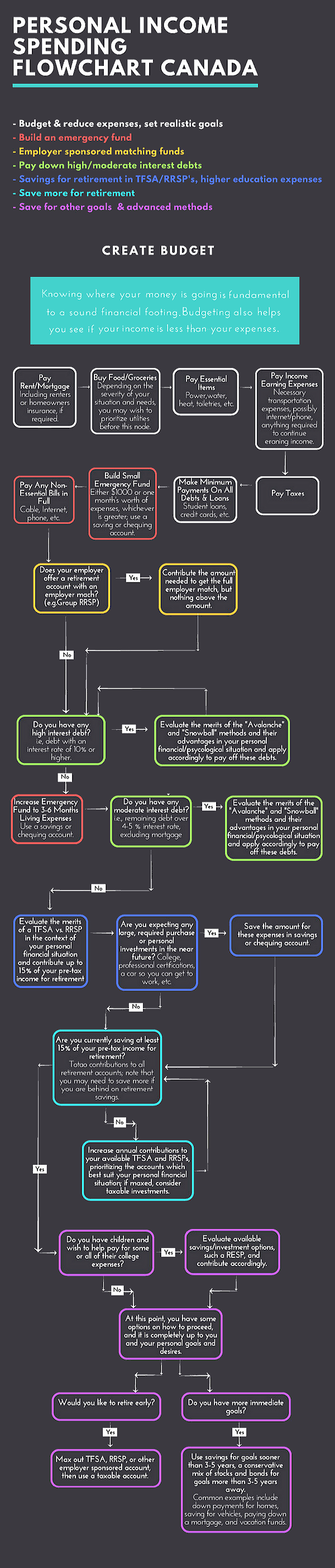

1. Budget and Reduce Expenses

The easiest way to start is to clarify your income and expenses. First, list down your sources of income: your salary, part-time or freelance job income, grants, rental income, etc. Then take a look at your expenses and list down what you spend on a monthly basis. To be effective in your budgeting, separate your expenses into two categories, and list them in order of priority:

Fixed Expenses: These are your recurring monthly expenses that are essential to your budget, including things like rent, key household utilities (power, water, heat, etc.) and spending on groceries (this would require you to determine a monthly budget for groceries, and stick to it!). This category also incorporates essential income-earning expenses (such as transportation, phone bill, and any other expenses that you require for work), as well as the minimum debt payments (mortgage, student loans, credit cards and other payments). If you cannot live without your internet, make sure to include it in your fixed expenses as well.

Variable Expenses: Variable expenses include purchases that do not necessarily occur every month, such as grooming, self and homecare, buying clothes for the change of the season, gifts, etc. It also includes non-essential monthly purchases outside of rent and major bills: paid memberships, subscriptions, etc. Entertainment and eating out can also be included in this category.

Take a look at the difference between your income and saving. If your spending amounts exceed your revenue, you have two options: 1 – to decrease your expenses, or 2 – to increase your income. A good place to start when you do need to be more conservative with your spending is managing your variable expenses. If nothing else can be cut there and you are still unsatisfied, then move to your fixed expenses and see which ones can be reduced.

2. Prepare for the Unknown

We all know that emergencies and adversities happen: we read about them on the news, hear about them from our friends, talk about them online. But do we go as far as to plan for unexpected situations?

Planning ahead is the second key step in budgeting.

Emergency “Buffer”: This is an essential step for any unexpected situations, such as a breakdown of a vehicle or an accident that requires additional medical, insurance or travel payments. An emergency buffer fund should have at least $1,000 in it, or one month’s rent (preferably the higher number). Please remember that an emergency situation does not include expenses that you knew about (ex.: yearly car maintenance) or things that you want, but did not budget for. It is strictly for emergency situations to give you peace of mind and to ensure that you do not accumulate any unnecessary debt.

Emergency Saving Account: Saving is always a good habit to have. However, here we are not talking about saving for a purchase or a trip – this is also an emergency account. Similar to the emergency buffer, this account is used in drastic, unexpected situations. The difference is that this account is bigger: it is set to cover large unexpected expenses, such as a sudden layoff or a financial crisis. Budgeting experts recommend saving at least 3 months’ worth of your income on this account; but it can go up to 9 months, depending on your income and saving habits, the competitiveness of your industry and your desired security level.

When it comes to an emergency account, you should prioritize the “buffer” and then work your way towards a stable emergency saving fund. You can have those two accounts together if that is more convenient.

3. Get Rid of the Weight

An average Canadian carries $22,125 in non-mortgage debt, according to Equifax report. As the average debt rates continue to grow, it becomes even more important to be mindful of your spending habits.

If you have already accommodated debt, especially high-interest debt, consider paying it off before you start investing or saving for the future. The rule of thumb is prioritizing your essential spending, then your emergency fund, and then debt payment; but it can be adjusted depending on your goals and needs.

There are several debt payment methods that you could consider:

Debt Avalanche: Avalanche method prioritizes paying off debts with the highest interest rate first while making minimum payments to others. Once the debt with the highest interest rate is paid off, you can start paying off the next high-interest debt. This is a great method for those who would like to pay less money on interest.

Debt Snowball: Snowball method focuses on paying off the smallest debts first while making minimum payments on the rest of the debts. Once the smallest one is paid off, you can reallocate those funds towards the second smallest debt, and so on until all debts are paid. This is an effective debt payment method for those who want to see progress in order to keep going.

If you need to be encouraged by the small wins in paying off your debt, but you also want to pay off the high-interest debts faster, you can combine those methods together.

4. Invest in Your Future

Once you feel like you are on track with your finances (you have a solid emergency fund and are getting ahead with your debt payments), you can and should start planning for the future.

Employer-matched RRSP: If your workplace offers a retirement plan that the employer matches, contribute the amount that you need to get the employer match, but do not exceed that amount.

Saving Acconts: Experts recommend contributing at least 15% of your pre-tax income into a Tax-Free Saving Account (TFSA) or a Registered Retirement Savings Plan (RRSP). Evaluate the merits of each account and make choose the one that suits your needs.

Future Goals: If you know that you have a large purchase coming up (for instance, a car purchase, etc.), start saving towards that purchase. You can also start planning for future family expenses (ex: helping your kids with their college expenses), or put more money into saving and investment funds.

Check out our Personal Income Spending Flowchart infographic to learn more about healthy budgeting habits!

The information contained in this post is considered true and accurate as of the publication date. However, the accuracy of this information may be impacted by changes in circumstances that occur after the time of publication. Ashton College assumes no liability for any error or omissions in the information contained in this post or any other post in our blog.